2026-02-02 · 6 min read

BeginnerStudent Banking Products in Canada: Accounts, First Card, and GICs

Learn the student essentials: pick the right account, build credit responsibly, and grow savings with guaranteed-return GICs.

Intro: what we’re doing here

If your bank account is basically “the place paycheques land… and then vanish,” you’re not alone. Student banking doesn’t have to be complicated, but the details do matter, and the banks do reel you in; especially the parts that quietly charge you fees or impact your credit score.

This guide is built for all students (college, university, mature, international) and focuses on the Big 5: RBC, TD, Scotiabank, BMO, and CIBC, as this is probably where you have an account established already. We’ll walk through the three main things most students need in the first place:

- An everyday account that won’t nickel-and-dime you,

- A first credit card that builds credit (without becoming debt),

- and a safe option like a GIC if you want guaranteed growth on savings.

We’ll also cover how student promos work, what fee traps to avoid, and what to do when you turn 18 (or hit age of majority in your province).

*Canada-wide note: Some details vary by province and age (for example, age of majority is 18 in most provinces and 19 in a few, i.e. BC + The Maritimes). Promotions also change often.

Everyday accounts

Junior vs. student vs. regular accounts

The first thing I want you to check is if you have the correct account type. A junior/youth account is usually meant for minors, often with parent/guardian involvement depending on the bank. A student account is built for post-secondary students and typically removes the monthly fee and increases everyday features like transactions and e-Transfers. If you don’t declare to the bank you are a student, they will switch you to a regular account, where you will have varying fees. So just check your online banking or make a call to your local branch.

Chequing vs. savings

Your chequing account is your daily operating system. It’s for debit purchases, rent, bill payments, and e-Transfers. Your savings account is where you keep money you don’t want to accidentally spend. Even if the interest rate isn’t mind-blowing, separating your money into “spend” and “save” makes budgeting easier without needing a spreadsheet for your life.

A good setup could be to keep a reasonable buffer in chequing so you don’t bounce payments, then move everything else into savings or a short-term goal bucket.

What to look for in a student chequing account

Most student chequing accounts are broadly similar, so you don’t need to hunt for a perfect match. What you want is a clean combination of: no monthly fee while you’re a student, enough transactions that you never think about them, and free Interac e-Transfers.

Chequing + Savings account combo, depending on your bank

- RBC: Advantage Banking for Students. This account has no fees for full-time students or anyone 24 years old or younger, no minimum balance, unlimited transactions and Interac e-Transfers. Paired with their High Interest Savings Account, 0.55% interest rate with no minimum balance. **DO NOT process transactions, pay bills or send e-Transfers with your savings account, they will charge you a fee!! They have an ongoing promotion that can earn you $100, you can see the account details here.

- TD: Student Chequing Account is a straightforward option built around “unlimited.” It is $0 monthly fee for students, includes unlimited transactions, and includes Interac e-Transfers. As for savings accounts, The Student Chequing Account does earn 0.01% interest, but their ePremium Savings Account earns 0.45% on balances over $10,000, whilst having no fees. Might be worth it if you fall into that category. Find the account details here.

- Scotiabank: Preferred Package for Students and Youth account is a 0 fee account that also includes unlimited debit transactions and unlimited e-Transfers. However, this differs from the other banks as you can also collect Scene+ points using this debit card. Pair it with the MomentumPLUS Savings Account that offers 0.40% interest, having a student chequing account boosts the interest to 0.45%. Scotia also has a signup bonus of $125 (*with terms and conditions), check out the product here.

- BMO: Student Banking product has 2 different tiers, where the Premium account is only free when you hold a minimum $6,000 in the account, or else it would be a $13.00/month fee. And the only benefits are you get a $150 rebate on a BMO Credit card. Or else, the product is similar to others, everything is free and unlimited. BMO also has a signup bonus of up to $175, but please read the fine print, you can find the details here. Their Savings Amplifier Account offers 0.50% interest!

- CIBC: Smart Start for Students + eAdvantage Savings combo is positioned as $0 monthly fee for students, with unlimited transactions including e-Transfers. The savings account offers 0.45% interest and a free SPC+ Membership. You can find these products here.

*The simplest takeaway: For most students, the best student chequing account is the one that (1) is truly no-fee, (2) has free e-Transfers, and (3) is convenient where you live and study. Switching banks for a tiny feature upgrade usually isn’t worth it unless you’re actively paying fees or your current bank is inconvenient.

**I would also like to highlight that both TD and CIBC both offer “Student Bundles”, which include a chequing account + savings account + credit card! I recommend checking them out.

Your first credit card

This card isn’t about rewards or perks, it is to build a credit history

Your first student credit card is usually not the one you’ll keep forever, but it will be your main credit builder at this stage in your life. When you eventually apply for better cards, a phone plan, a car loan, or even some rentals, credit history can matter. You don’t need to be a credit wizard, you just need a clean track record!

The three rules that matter most

The simplest strategy is the best strategy. First, pay on time every month, no exceptions. Second, keep your balance low relative to your limit (this is utilization, remember the 30% rule). Third, avoid carrying a balance because credit card interest is expensive and adds up faster than most people expect. If you’re worried about forgetting, set autopay for at least the minimum payment, and then manually pay the rest.

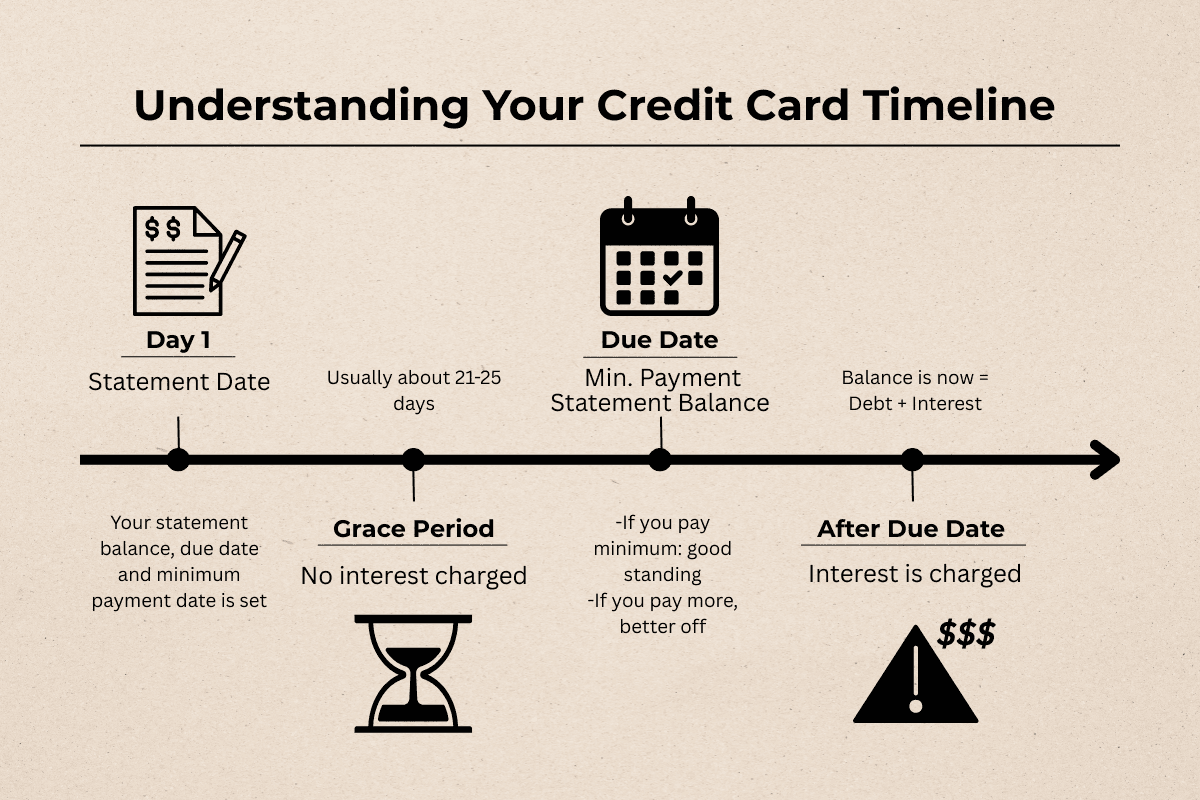

Statement date vs. due date

Your statement date is when your monthly bill is created. Your due date is when it has to be paid. In most cases, if you pay the full statement balance by the due date, you avoid interest on purchases. Keeping these dates in mind is crucial.

Big 5 student credit cards

- RBC: The ION+ Visa card is going to be your best pick, especially if you have the Advantage Banking account mentioned above as the annual fee ($48) is waived. This card offers 3x Avion points on grocery, gas, dining, food delivery, rideshare and streaming services, along with 1x points on everything else. Not a bad starter card at all. If you don’t have the banking product, the ION Visa card is free but only offers 1.5x points on the categories listed above. View the ION+ here.

- TD: TD’s student credit card is called the TD Cash Back Visa and from the name, yes it offers cashback instead of reward points. This cashback rate is 1% on all purchases, and this card has no annual fee. Details here.

- Scotiabank: Scotia actually offers 5 different student cards for some reason. There are 3 of them that are 0 fee, and 2 that have a low annual fee. They offer cards with reward points, cashback (2 tiers), low interest and an American Express card, so choosing the right one will be up to what you prefer to get out of the card, you can riffle through the options here.

- BMO: Their only student product is a BMO CashBack Mastercard, which offers 3% cashback on groceries, 1% back on recurring payments (automatic payments like phone bills, streaming services, etc) and 0.5% back on everything else. No annual fee. To be honest it isn’t horrible if you are a BMO customer. Info here.

- CIBC: CIBC also offers 5 different student credit cards: 2 cards with different reward point systems, an Aeroplan card and a cashback card. If you are more inclined to travel rewards, then choose the Aeroplan or the Aventura card, or else I would recommend the Dividend Visa card. Do not get the CIBC Classic Visa card, the other options are far better. Check out the options here.

One-card rule: You don’t need multiple student credit cards to “build credit faster.” One is enough. Build a clean payment history, keep balances low, and you’ll be in a great spot later.

GICs (Guaranteed Investment Certificates)

What a GIC is explained like you’re 5

A GIC is a guaranteed deposit investment. You put money in for a fixed term (i.e. 1, 3, 5 years) and the bank pays you a set return. At the end, you get your original deposit back plus the interest earned. The catch? It is locked. You cannot cash in or add more into the account.

Why students should care

GICs are useful when the goal is when you tell yourself “I cannot lose this money”, or want to keep some cash locked away to break temptation. Think tuition for next term, a planned move, a car fund, or savings you want to protect. They’re also especially relevant for students under 18 who can’t invest in markets yet, because a GIC lets your money earn something while staying low risk. I did this myself before I can open an investment account!

Registered vs non-registered GICs (quick overview)

You can hold GICs in registered accounts like a TFSA or RRSP (and sometimes FHSA/RESP), depending on eligibility and what you’re using the money for. This matters because registered accounts have that tax shelter, but will use up your contribution room. It isn’t worth the small return. And yes, that means that GICs from a bank are considered taxable income.

Big 5 GIC offerings (high-level)

All five banks offer both basic GIC types, with a range of terms and purchase options through online banking or in-branch. They may offer different interest rates, so do your research. You are free to shop around and open your GIC with a new bank, it won’t affect the interest rates!

Turning 18 checklist

When you turn 18 (or hit age of majority in your province), your banking life gets more “independent,” and it’s worth doing a quick reset.

- First, confirm your account is the student version and won’t quietly convert you into monthly fees.

- Third, if you’re getting a credit card, start with one student card and set autopay immediately so you don’t accidentally miss your first payment. The earlier you start the better, even if you are barely spending.

- Finally, separate your savings from spending, whether that’s a basic savings account or a short-term GIC for money you don’t want to touch.

Post-grad note: Student status doesn’t last forever. Make a yearly reminder to check whether your account will convert after graduation or at a certain age. However most banks are saying 24-25 years of age.

Closing notes

Student banking isn’t about having the best bank, but about having a setup that avoids fees, builds credit cleanly, and makes saving easier without thinking about it every day. If you do one thing right now, log into your banking app and confirm you’re on the correct student plan. It’s the simplest change that can save you the most money.

TL;DR

- Everyday banking: Make sure you’re on a student chequing plan (so you’re not paying monthly fees for no reason).

- Chequing vs savings: Use chequing for spending + bills, and savings for money you don’t want to accidentally spend.

- Must-have features: Prioritize free e-Transfers, enough/unlimited transactions, and ATM access if you care.

- Promos: Treat promos as a bonus, ALWAYS read the conditions.

- First credit card: Get one starter student card to begin building credit, rewards are secondary!

- Credit rules: Pay on time, keep your balance low vs your limit (utilization), and avoid carrying a balance to dodge interest.

- Statement basics: Pay the statement balance by the due date to typically avoid purchase interest.

- GICs: A GIC is a safe, guaranteed-return option when you won’t need the money for a set period.

- Turning 18 checklist: Confirm student status, turn on alerts, decide on overdraft, set autopay, and separate spending vs saving to avoid surprise fees.

Disclaimer

This is educational content and not financial advice. Bank products, rates, eligibility rules, and promotions can change and may vary by province and personal circumstances. Always verify details with the bank before opening or switching accounts.

Leave feedback

Anonymous and quick — your thoughts help shape future guides.

Recommended next reads

9 min read

Tariffs, Trade Wars, and Your Money: What Actually Happened and What to Do Now

A plain-English breakdown of 14 months of Canada-US tariffs: what triggered it, what it actually did to prices and jobs, and three things worth doing with your money right now.

10 min read

Credit Cards 101: The Right Card, the Right Habits, the Right Order

Most people learn how credit cards work by getting it wrong first. This is the breakdown that skips that part: how interest compounds, what your card does to your credit score, and which Canadian cards are actually worth carrying.

5 min read

Understanding Your Student Loans (Canada): The No-Stress Guide

A friendly guide to how Canadian student loans work: federal vs. provincial, interest rules, grants, grace period, and repayment; so you can handle it without spiraling.